When we look for the different types of banks that are present in India, we mainly see either the bank is a Private bank or Public Sector bank. However, when we start to understand the different banks, we get to know that there are multiple types of banks.

Here is the list of different types of banks in India:

- Central Bank

- Commercial Banks

- Co-operative Banks

- Regional Rural Banks

- Small Finance Banks

- Payment Banks

- Local Banks

- Specialised Banks

Central Bank (RBI)

Every country has only one Central bank which governs all other banks and financial institutions across the country. In case of India, Reserve Bank of India (RBI) is the Central Bank of India, which is headquartered at Mumbai. RBI has total control over functionality of other banks.

Functions of Central Bank:

Government’s Bank

The fundamental duty of RBI is to act as government’s bank and accept deposit from government as well as provide interest on those deposits when required. There are times when RBI prints money when advised by government. RBI also issues fund for state governments when required.

Currency Issuer

RBI is the only institution that can print currency all over the country. RBI has mandate to print currency notes as well as mint coins when deemed necessary. All those coins you used in payphones to talk when there were no mobile phones are minted by RBI. Every currency note you use is printed at RBI.

Implementer of monetary policies

RBI is given exclusive rights to impose the monetary policies throughout country. It imposes these policies by issuing guidelines to other banks. RBI has multiple tools to control monetary policies such as Cash Reserve Ratio, Repo Rate and Reverse Repo Rate. These monetary policies are crucial to control inflation in country as well as bring liquidity in money market when necessary.

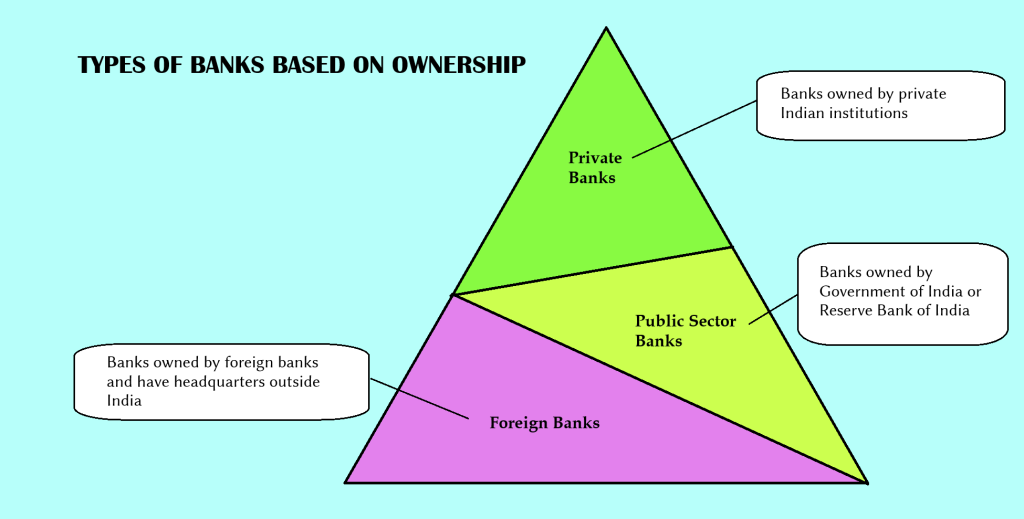

Commercial Banks

These banks are recognised under the Banking Companies Act, 1956. These banks are known as commercial banks ass their main objective is to generate profits. These banks operate on commercial basis.

There are different types of banks which can be owned by either government or private players. These banks get their source of funding from public funds. Most of these banks serve all types of customers irrespective of whether the customer belongs to retail segment or institutional segment.

Still many banks have preference as banks such as HDFC Bank have preference towards retail customers while banks such as ICICI Bank have preference towards Industrial customers. Many banks focuses on only rural customers while other banks have preference towards urban population.

Moreover, commercial banks can be segregated into three categorises:

- Public sector banks

- Private sector banks

- Foreign banks

Public Sector Banks

These banks are owned or has majority stake of government of India or its majority stake is covered by Reserve Bank of India.

Below is a list of Public Sector banks

Private Sector Banks

These banks have their majority owned by private institution or individuals or group of people.

Below is a list of Private banks

Foreign Banks

These banks are owned by foreign entities and they have headquarters outside India. Most of these banks target high net worth individuals.

Below is a list of Foreign banks

Co-operative Banks

These banks operate under license from State government. The main objective of such banks is to promote welfare of society. Therefore, these banks disburse low interest loans to their clients. Most of these loans are focused on agricultural business such as farming and selling agricultural products.

There are different types of Co-operative banks present at different levels which are state level, district level and village level.

State Level Cooperative Banks [TIER – 1]

These banks are regulated by State government, RBI and NABARD. The funding is also made by RBI, NABARD and State government.

The regulations are almost similar to commercial banks such as CRR being 3% and SLR being 25%.

District Level Cooperative Banks [TIER – 2]

These banks are governed by State government and RBI do not have much control over them. These banks provide services to semi-urban population.

Village Level Cooperative Banks [TIER – 3]

These banks are village level where they are regulated by State government and its governing body members are mostly village panchayat members.

Regional Rural Banks (RRBs)

RRBs are agricultural focused banks that provide loans in more affordable rates to farmers. These banks are joint ventures between central government (50%), state government (15%) and a commercial bank (35%). The process of establishing RRB banks started from 1987 and went on till 2005. There were almost 195 RRB banks established which were reduced to 82 till date. RRB have limitation that they can open branches in only 3 geographically connected districts.

The main objective of these banks are following:

Financial Inclusion

The objective remains to bridge the gap between rural banking system and urban banking system. These banks are focused on rural population to bring them in jurisdiction of financial inclusion by providing them with financial services.

Credit Access

Most people in rural areas remain below poverty line due to lack of financial support. These banks provide rural people with low interest loans that can help farmers, labourers, artisans and small business owners. Before banks, loans were provided by moneylenders who would charge exorbitant interest rates on loans.

Government Scheme Disbursement

Regional Rural Banks works as facilitators for government scheme fund transfer to eligible people. Citizens who have chosen to obtain various financial facilities under government schemes need to open account in RRBs. Since account is opened with Aadhar verification, payment reaches genuine people only.

Small Finance Banks

These banks are governed by Reserve Bank of India (RBI) and caters to need of Micro, Small Medium Enterprises (MSME) and agricultural industry related customers. These are different types of banks in comparison to commercial banks as they are mostly private owned banks where lower interest loans are available. Moreover, the interest rates for savings and term deposits is higher when compared to commercial banks.

Following are the currently recognised small finance banks:

1 Utkarsh Small Finance Bank

2 Spandhhan Small Finance Bank

3 Ujjivan Small Finance Bank

4 AU Small Finance Bank

Payment Banks

These are a new form of banks that RBI conceptualised considering the requirement of people to open bank account quickly within hours to complete transactions.

Normal banks are different types of banks when compared to Payment banks as more stringent checking are conducted on customers. In a commercial bank, Aadhar authentication is required to open a bank account.

When considering deposit amount, Payment bank account can only hold upto ₹ 1,00,000 /- while compared to payment banks, other different types of banks have no such limit on capital that your account can hold.

When considering location of banks these totally are different types of banks as they are mostly online banks with no exact location of bank branch. However, few banks have gone far and build few branches for customers to visit.

Payment banks compared to other banks do not provide financial services such as loans facility or credit card facility which is widely used in commercial banks.

In these banks, customers are given services such as online banking, mobile banking as well as ATMs.

Following are few of these payment banks:

1. Indian Post Payment Bank

2. Airtel Payment Bank

3. Jio Payment Bank

4. Paytm Payment Bank

Local Area Banks

Considering the issue of lack of capital flow in rural India, government decided to bring Local Area Bank concept where the local money keeps flowing in the rural areas which boost the economy of rural India.

Currently, there are only two active Local Area Bank operating in India. One of those is Coastal Local Area Bank (Andhra Pradesh) and the second one is Krishna Bhima Samruddhi Local Area Bank ( Telangana). Any bank considered as Local Area Bank need to be a private bank and registered under Companies Act, 1956. These banks are not financed by government and therefore are profit focused banks. However, Local Area Banks are also focused on community development and improving the financial inclusivity of people. Such banks provide community with health care services as well as providing education to poor people.

However, there are many banks that earlier fell in Local Area Bank category have upgraded into Small Finance Bank and started expanding their target location to urban and semi-urban areas.

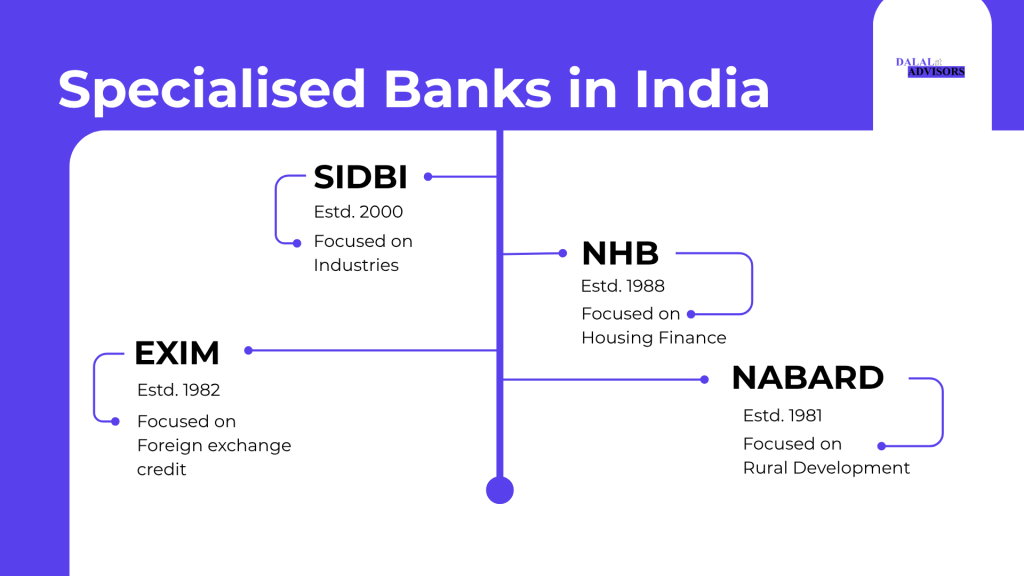

Specialised Banks

Specialised Banks are banks that were implemented by Government to focus on financial systems other than common public. Most of these banks provide different types of services that are not related to common public issues. Some of the functionalities include generating foreign trade credits, finance for heavy industries, improving infrastructure through financing. Special banks also provide financing for housing targeting housing projects where the promoters are provided with financing.

These banks are like unsung heroes among different types of banks in India. Many people do not have any ideas about these banks and their purposes. Let me mention few of the specialised banks that play special role in our economy.

1. NABARD

The NABARD stands for National Bank for Agriculture and Rural Development. The bank was first established in 1981 under the NABARD Act, 1981. Before NABARD, the agricultural finance was overseen by RBI alongside Agricultural Refinance and Development Corporation (ARDC).

The main functions of NABARD include development of Self-help groups (SHGs). SHGs mostly comprises of poor women who do not get any kind of access to finance from banks. SHGs form backbone of many villages where there is no access to banks. These SHGs work as bank and provide credit to women members when they need it thus bringing financial power to those women.

NABARD also plays the role of statutory inspector for rural banks and cooperative banks. NABARD conducts statutory inspection of Regional Rural Banks (RRBs), District Cooperative Central Banks (DCCBs) and State Cooperative Banks (StCBs).

2. SIDBI

Small Industries Development Bank of India (SIDBI) was initially a part of IDBI bank. However, in 2000, it was de-linked from IDBI. Its main purpose is to provide finance to banks and financial institutions that only engage in financing industries. It is considered as the principal financial institution in the Micro, Small and Medium Enterprises also known as (MSMEs).

Recently, it brought out an index that measure the sentiment of MSE sectors. The index was introduced in collaboration with CRISIL.

3. EXIM

In an increasingly interconnected global marketplace, international trade requires more than just high-quality products; it demands sophisticated financial backing. The Export-Import Bank of India (EXIM Bank), the apex financial institution established in 1982 to lead the nation’s cross-border commerce. Operating as a strategic catalyst, EXIM Bank has evolved from a traditional export credit provider into a major engine driving India’s integration into the global economy.

EXIM bank has multi-dimensional role that includes supporting small enterprises as well as large conglomerates in managing foreign reserves and meet other foreign related needs such as:

- Lines of Credit (LOCs): Channeled to overseas governments and financial institutions to encourage the import of Indian goods and services.

- Buyer’s and Supplier’s Credit: Financing structures designed to lower risk and make Indian exports highly competitive in international bidding.

- Corporate Banking: Tailored term loans for Indian companies aiming to set up joint ventures or acquire assets overseas.

EXIM bank also has a department that exclusively conducts research on foreign trades and environment focused on business in other countries to give companies a lookout about good and bad scenario across business world through the world. Such complex information helps Indian companies to plan their future moves synchronising with the geopolitical shifts of India. These reports are quite helpful for exporters to focus on emerging markets for their products.

The bank’s active alignment with national economic priorities like the “Make in India” initiative help in making decisions that ultimately helps in growth of financial power of country. EXIM Bank acts as a financial bridge, enabling homegrown industries to scale globally while safeguarding them against international payment risks.

EXIM bank acts as institutional backbone for exporters, financial professionals and large conglomerate as it helps fuelling the growth ambition through international trades. It helps MSMEs through various initiatives including “Ubharte Sitaare”” programme where trade assistance is provided and export factoring is presented in simplified manner.

EXIM bank is focused on creating better competitiveness for India through using means such as providing term loans, import finance, Guarantees and Line of Credits and Export facilitation.

4. NHB

Shelter is one of humanity’s most fundamental needs, yet building a robust, accessible housing infrastructure requires a specialised financial blueprint. Concerned about future housing finance and affordable housing for all, government created National Housing Bank (NHB). This apex development finance institution was established in 1988 under an Act of Parliament to spearhead India’s housing finance sector. Wholly owned by the Government of India, NHB serves as the structural backbone that channels liquidity into the residential real estate market, transforming the vision of affordable housing into a reality for millions.

NHB does not deal directly with retail retail customers or issue individual home loans. Instead, its primary systemic functions include:

- Refinancing Powerhouse: Providing low-cost, long-term credit lines to Housing Finance Companies (HFCs), scheduled commercial banks, and regional rural banks to keep mortgage markets liquid and competitive.

- Market Intelligence via NHB RESIDEX: Managing India’s first official housing price index, tracking residential property inflation and price anomalies across major cities to guide developers, lenders, and policymakers.

- Supervisory and Developmental Oversight: Working in tandem with the RBI to audit, inspect, and enforce strict prudential norms across HFCs, safeguarding the sector against systemic risks.

Furthermore, one of the most crucial role of NHB is implementation of state-sponsored welfare programs related to housing. These includes affordable housing funds and urban infrastructure development schemes. By bridging the gap between formal capital markets and lower-income households, NHB ensures that credit reaches underserved rural and semi-urban territories.